Why Your Gas Isn't Getting Cheaper

A war has blocked a fifth of the world's oil. The price fell back anyway. One of them is a lie, and it's showing up at your pump.

My ten-year-old spotted it before Wall Street did.

For about a week, the oil war had been the only story on the evening news, and my daughter kept asking me what it all meant. So I did what you do with a ten-year-old. I turned it into a story about milk.

Every night I'd add a little more to it. And then one night she looked up and asked me a question so sharp it stopped me cold, because it's the exact same question the smartest, best-paid people in the oil market are staring at right now, and most of them are getting it wrong….

I've spent the last few months buried in this market the way I've only ever buried myself in a handful of genuinely world-changing events. I've read the reports. I've watched the jawboning. I understand the inventory and critical levels around the world…. And I keep coming back to a disconnect so large, and so strange, that once you see it you can't unsee it.

My daughter saw it in about ninety seconds.

Let me tell you the story the way I told her, so you see it too. I promise we’ll bring it into real oil info and it'll land by the end.

She asked me why the milk cart never comes anymore.

Let me explain.

Here's the story I'd been telling her.

Imagine a town where all the milk arrives on a single road. Every morning, a cart rolls down that road into the city, and everyone gets their milk. When the road is open, life is good. The people are so happy they practically jump for joy.

Then one day, soldiers block the road. They plant a stop sign, and the cart can’t get through. The milk just sits there, on the wrong side. And the people in the city are left waiting, confused, upset, with nothing coming.

That’s happening in the real world right now.

Except it isn’t milk.

It’s oil.

Late February 28 2026, a war broke out in the Middle East, and it blocked a narrow stretch of water called the Strait of Hormuz, a channel so important that roughly a fifth of all the oil on Earth has to sail through it.

It’s the one road.

And it got blocked.

When the only road into town gets blocked, the price of milk goes up.

This is the part even a child understands instantly.

Less milk coming in means the milk that’s already here becomes precious. The price climbs. Nobody has to explain it. It’s just how the world works.

And for a while, that’s exactly what oil did. It nearly doubled. The global benchmark, a type of crude called Brent, rocketed from about $72 a barrel before the war to $126 at its peak.

That single month was the biggest one-month jump in the entire history of the oil market.

The milk-road logic held perfectly.

Which is what makes what my daughter asked next so unsettling.

So why has the price of oil fallen back to where it started?

That was her question. Not in those words, of course. What she actually said was:

“Daddy, if the road’s still blocked... why isn’t the milk still expensive?”

Because that’s exactly what’s happened.

Today, crude oil trades right back around where it sat before the war ever began, before a single ship was turned away, before the first shot was fired.

The price is behaving as if the milk cart is rolling merrily into the city again, full to the brim, and the whole town is jumping for joy.

But the road is still blocked.

The soldiers are still standing there.

Almost no oil is actually getting through.

She caught it instantly, the thing that didn’t fit.

A ten-year-old’s logic couldn’t reconcile it, and neither can mine.

Both things can’t be true. One of them is a lie.

Either the milk is flowing, or the road is blocked.

It cannot be both.

That single contradiction is the whole story. It’s what my daughter saw in a heartbeat, and it’s what an entire market of highly-paid professionals is currently talking itself out of believing.

So which one is the lie?

Let me show you, one piece of evidence at a time.

You don’t need to know anything about charts. I’ll walk you through each one like we’re standing at your kitchen table.

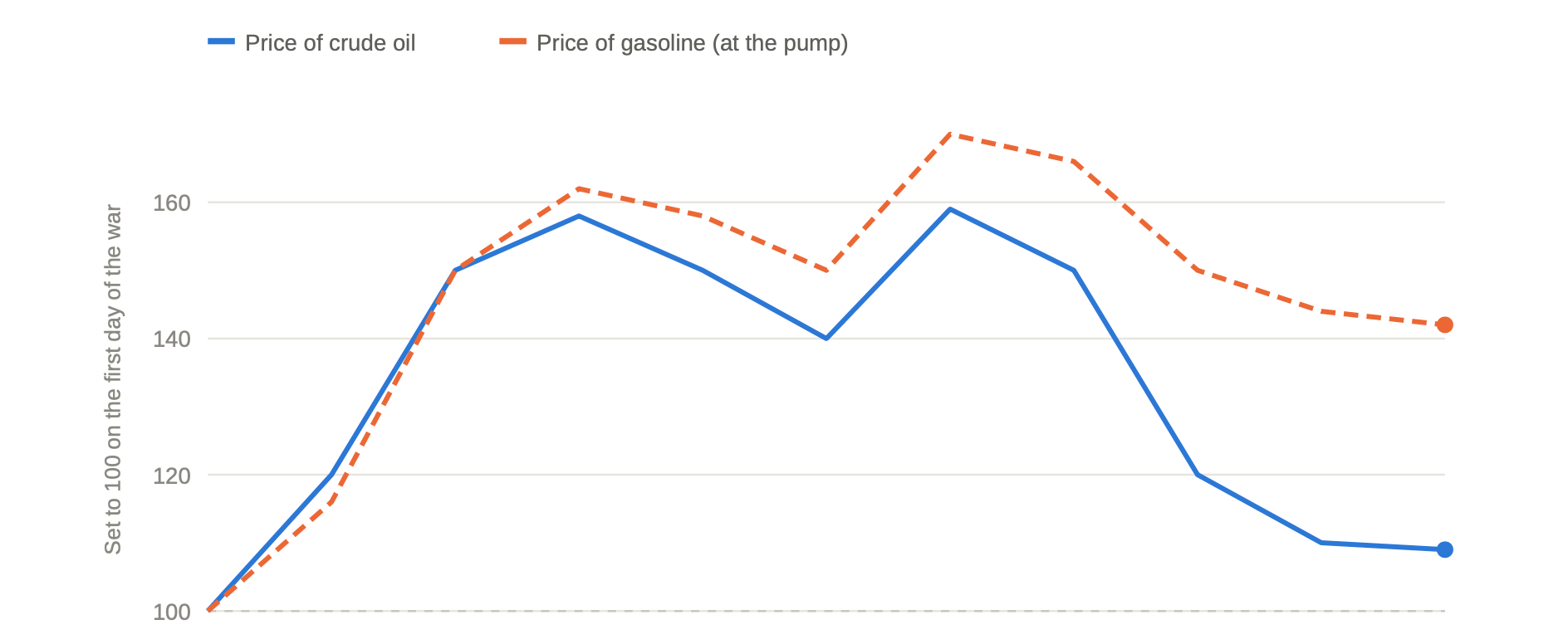

Here’s the first crack in the story: oil went home, but your gas didn’t follow it

Look at this.

It’s the simplest chart in the world.

It takes two prices, the price of crude oil, and the price of the gasoline you pump into your car, and lines them up starting from the day the war began. To make them easy to compare, we set both to “100” on day one.

If a line climbs to 150, that thing got 50% more expensive.

If it falls back to 100, it’s right back where it started.

Watch what happens. Both lines leap up together when the war hits, exactly as you’d expect. Then the crude oil line comes almost all the way back down, nearly to 100, back home.

But the gasoline line, the number that hits your wallet every week, refuses to follow it down. It just hangs up there.

If the world were truly re-supplied with oil, the pump would drop right alongside crude. It hasn’t.

Which means something in the middle, somewhere between the barrel and your gas tank, is still badly, badly broken.

And to see what, you have to understand one small thing about how oil becomes gas.

The reason hides in a number almost nobody watches.

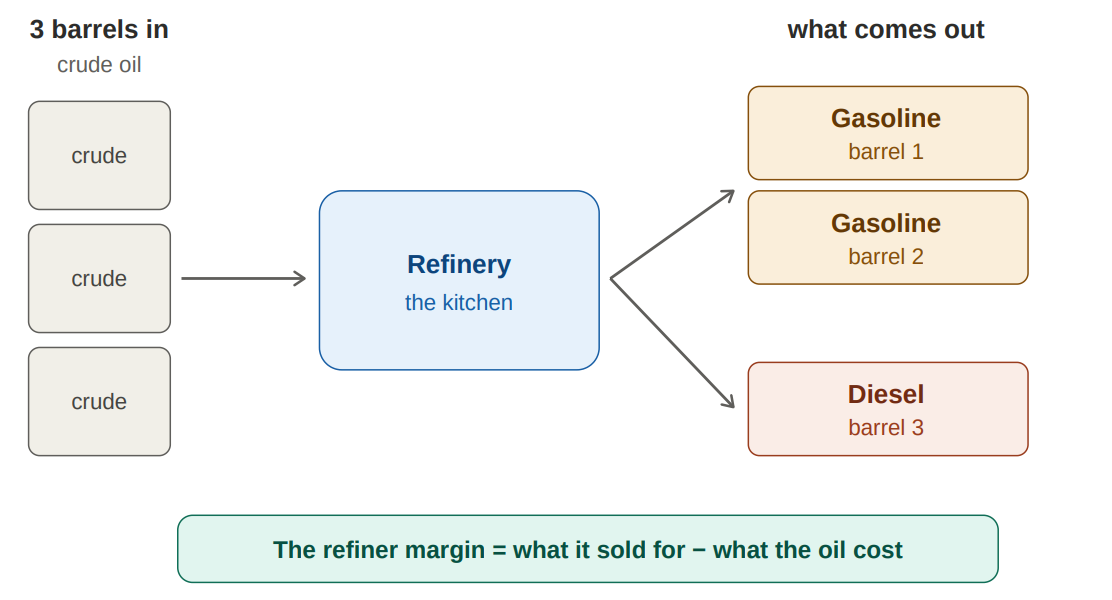

Here’s the thing nobody tells you: you don’t actually burn oil.

Crude is thick black goop straight out of the ground. Useless as-is. Before it can do anything, it goes to a factory called a refinery, which is really just a giant kitchen. Goop in one side. Gasoline,diesel, and jet fuel out the other.

Think of a dairy.

Raw milk in one door, bottles of milk and tubs of butter out the other. And the dairy makes its money on the gap, the difference between what it pays for the plain raw milk and what it sells the finished bottles for.

Refineries live on that exact same gap. Traders even have a name for it. They call it the crack spread. There's a standard recipe for it, the "3-2-1": take 3 barrels of crude, and a normal refinery turns them into about 2 barrels of gasoline and 1 barrel of diesel. The crack spread is just what those finished products sell for, minus what the crude cost.

FOR THE TRADERS everyone else can skip this On a screen, the 3-2-1 is three futures contracts: crude (CL, priced per barrel), gasoline (RB), and diesel/heating oil (HO). The catch: the products are quoted per gallon, and there are 42 gallons in a barrel, so you multiply each by 42 to convert to dollars-per-barrel. Recent prints: CL ≈ $68.63, RB ≈ $2.9189/gal, HO ≈ $3.1747/gal. Run the recipe (2 gasoline + 1 diesel, minus 3 crude): (2 × 42 × 2.9189) + (42 × 3.1747) − (3 × 68.63) = 245.19 + 133.34 − 205.89 = $172.6 total across the three barrels. Divide by 3 → ~$57.5 a barrel. That's identical to the symbol -3*CL + 84*RB + 42*HO (the 84 is just 2 × 42), which prints ~172 and ÷3 gives ~$57. Same number, three different ways. This isn't a rounding artifact; it's the tightest refining margin on record.

Almost nobody outside the industry watches this number, because for years it’s been boring. In a normal world, a refinery makes maybe $15 to $25 a barrel on it, and it barely moves.

Now brace yourself.

Right now, that number is the highest it has ever been in history.

About $57 a barrel. More than double its normal level. An all-time record.

And here’s the part that should stand every hair on your neck up straight: it broke that record while crude oil was falling.

You don't need to read a single wiggle. Just look at this chart in three glances.

Before the war, on the left, the refiner's cut is that black line down at the bottom. Boring. Ordinary. A calm, normal world.

The war hits, and the black line launches straight to the top. Something broke that day and never healed. And on the far right edge, right now, the price of crude is sliding back down, but that black line is climbing back up to a fresh, brand-new record high.

Sit with that for one second, because it's the entire story compressed into one picture.

The raw ingredient is getting cheaper.

But the finished product, your gasoline, is so scarce that the middleman's cut is the fattest it has ever, ever been.

Which means the fuel itself, the stuff in your tank, is running dangerously short.

Because those two things, cheap crude and a record refining margin, only ever move in opposite directions when the actual finished fuel is critically scarce. And there's a way the pros double-check it.

If you work backward from how tight the gasoline and diesel markets really are, they imply crude oil "should" be trading somewhere between $100 and $125 a barrel right now.

Not the $68 on the screen.

Two completely different methods, same answer.

The screen price of crude is the odd one out.

Here's where it touches your life, and the news. Not long ago the President went on social media, accused the oil companies of "gouging" you, and told the Justice Department to investigate them for not dropping prices at the pump. But the industry's reply was, essentially, a crack-spread lecture: gasoline doesn't move in lockstep with crude during a supply crisis that's still choking off refined fuel.

They were right.

That fat $57 isn't greed. It's a flashing scarcity light, glowing exactly where the textbook says it should. The oil companies practically warned this would happen. So now you know what's strange.

The real question is why?

So why is the price still calm? Four reasons, and they all point the same way.

If the physical world is this tight, why is the headline price of crude sitting there calm as a millpond?

There are four reasons. They braid together into a single story. And every one of them points the same direction. Take them one at a time.

One: the road really is still blocked. The ships prove it.

Forget the headlines. Forget the handshakes. Watch the actual boats.

For most of this crisis, traffic through the Strait of Hormuz has run at roughly 5% of what it was before the war. On the days anything moves at all, it's mostly Iranian tankers and a shadowy fleet of sanctioned ships, creeping along a route Iran controls, paying Iran a fee, through water that may still be sown with naval mines.

Meanwhile, something like 6 million barrels a day of oil production sits shut off completely, wells simply switched off across Saudi Arabia, Iraq, Kuwait, and Qatar, because their oil physically cannot get to market.

Let me put that number in perspective.

If this were a normal market, a 6-million-barrel-a-day outage would be the single largest oil supply disruption in the history of the world. Bigger than the 1970s.

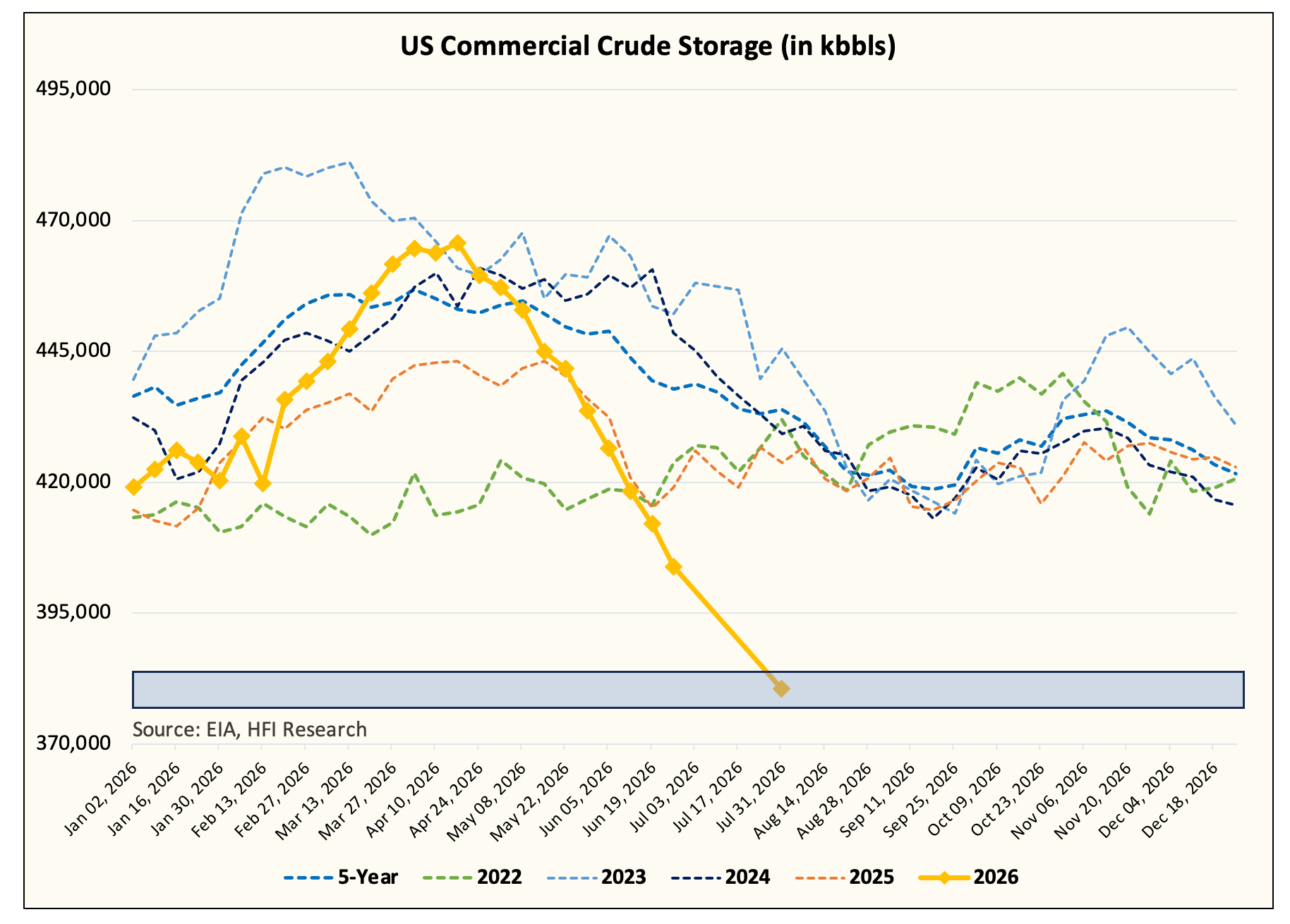

And to cover the hole, the world has been quietly draining its stored-up reserves at more than 35 million barrels every week, week after week after week. America's own commercial oil stockpiles aren't just low; they're falling in a near-vertical line straight through the floor of anything seen in five years.

Source: HFI Research

The milk cart, in other words, is still very much stuck behind that stop sign

Two: every trader on Earth has leaned to the same side of the canoe.

This is the mechanical reason the price is low, and it has nothing to do with actual barrels. It's about betting.

There's a group of big professional traders, hedge funds and the like, whose bets get tallied up every week in a public report called the Commitment of Traders. It's how you see which way the herd is leaning. And right now, that herd is betting on lower oil prices about as hard as it has in twenty years.

How hard?

By one measure, this level of bearish betting sits in roughly the bottom 2% of every reading going back to 2011.

The only company it keeps is genuine catastrophes, the 2020 pandemic crash, the 2015 oil collapse. Everyone has piled onto the same side of the canoe to bet the price keeps falling.

Now think about what that actually means.

When everybody has already placed the same bet, there's nobody left to place it again.

The selling is used up. And the moment the price so much as ticks upward, all those people leaning off one side have to lunge to the other side at once to keep from capsizing.

That lunge is buying.

And it can heave the price up violently. A crowded bet like this doesn't sit there safely. It's a coiled spring. As one sharp analyst I follow, who writes under the name PauloMacro, put it: the market is happy to say oil's price reflects today's scarcity when crude is at $100, then turns around and prices in some future glut to justify $70.

You can't have it both ways.

Three: the biggest buyer of oil on the planet quietly walked out of the room.

This is the part almost nobody at the dinner table knows.

And it's the real reason the screen looks so calm. Back in April, the single largest buyer of oil on Earth, China, simply stopped showing up.

It cut its purchases by something like 4 to 5 million barrels a day.

The world's biggest customer walked out of the store…..

And that one move, one enormous buyer stepping back, was almost precisely enough to cancel out all that shut-off Middle Eastern supply….

Fewer barrels being pumped, yes, but also a giant buyer no longer competing for them.

The two roughly offset.

And the paper price stayed calm.

So…..How could China afford to just stop?

Because it stocked up first.

While everyone else's reserves now collapse, China's sit near record highs. It filled its tanks before it stepped away, and it's been living off that hoard ever since, running its own refineries slower to stretch it out. But, and here's why this matters more than anything else in this whole piece, China can't do this forever.

Its own supplies of finished fuel have been draining hard for months, toward levels its government won't want to test. And with Middle Eastern refineries knocked out by the war, China happens to hold the only large chunk of spare refining capacity left on the planet, roughly 7 million barrels a day of it. The world increasingly needs China to fire those refineries back up and start buying crude again.

And there are early signs it's beginning to.

The world's largest independent oil trader, Vitol, said it plainly. As their CEO Russell Hardy put it, all of the world's spare capacity now sits behind the Strait of Hormuz, so the impact is direct. The cushion everyone assumes will save them is locked on the wrong side of the blockade.

"Today, all of the spare capacity is behind the Strait of Hormuz, so the impact is obviously very direct."

— Russell Hardy, CEO of Vitol, at the FT Commodities Global Summit in Lausanne

China has lately been the aggressive buyer hoovering up oil stored on tankers around Asia, and doing much of the buying that's already cut the oil stranded behind the Strait of Hormuz roughly in half.

So the entire oil market is holding its breath, waiting to see what one giant decides to do.

The research shop HFI Research framed it better than anyone: the rest of us, all the traders and analysts counting our little barrels, are nothing but ants in a field full of giants.

And nobody, not even the pros, knows exactly why.

Here's the wrinkle that keeps serious people up at night.

Why is China still not buying in size, even now that it would be profitable to do so? Nobody actually knows. China is a black box, and it always will be.

HFI raises one possibility, carefully, and I'll hand it to you exactly the way they hand it out, as a maybe, not a fact. What if China used this war as cover to run an experiment? What if it deliberately choked off its own seaborne oil for months, on purpose, to find out whether its economy could survive a blockade, the very kind it would face if it ever moved on Taiwan and the West cut its supply lines in return?

A dress rehearsal, disguised as a trading decision.

HFI is the first to call this "tinfoil hat" territory, and I'll echo that.

It may be nothing. But the mere fact that sober, barrel-counting oil desks are seriously wondering about it should tell you how far past normal supply-and-demand this market has drifted. The giant's motives are unknowable. We just have to watch what it does.

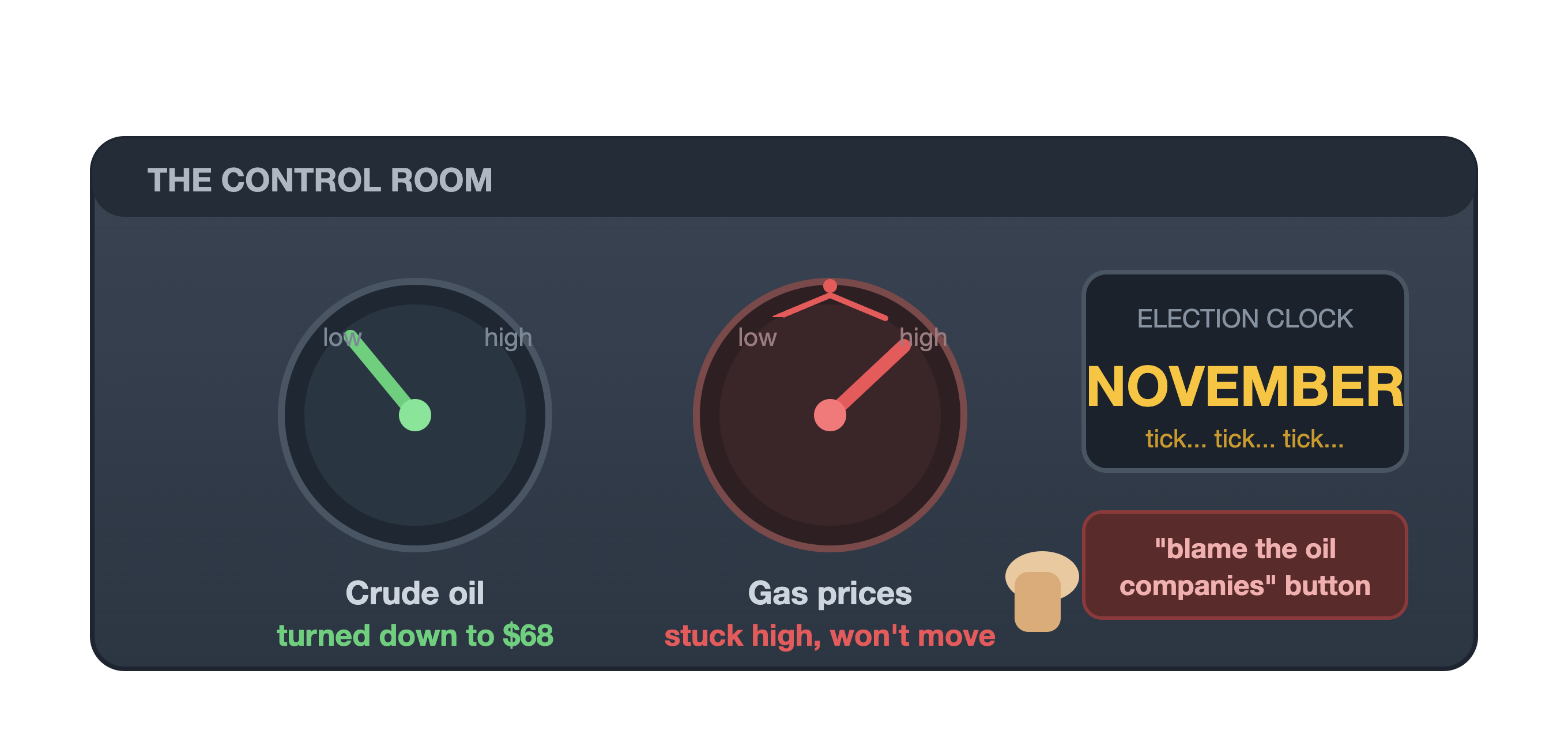

Four: the one man who could fix it has trapped himself, with an election clock ticking.

There's a last reason the price has stayed pinned down, and it's the most human one.

It's being talked down.

The President has proven remarkably good at using words alone to shove oil lower. Traders gave the pattern a nickname during his tariff fights: TACO, "Trump Always Chickens Out." Make a terrifying threat, spook the markets, then reverse course right before they open and declare victory. It worked back then because a tariff is a switch you flip with a single post.

But a war is not a switch.

Traders have a sequel nickname for this one: NACHO, "Not A Chance Hormuz Opens." The rhythm has been almost theatrical, an ultimatum rattles oil over a weekend, then minutes before the market opens a "deal" gets announced and the price drops. One tally found the President claiming a near-agreement to end this war at least 38 separate times since March. Each headline nudges the price down. Not one has moved a meaningful number of ships.

And here is the box he's built around himself, which is also the clock on this entire story. Gas prices are poison in an election year, and a midterm election is coming this November. Polls show most Americans blame him for what they pay at the pump. Swing voters on tight budgets are openly telling reporters a $4.96 fill-up will change their vote.

So the White House desperately needs gasoline cheaper.

Now.

But it can't deliver.

Because the thing keeping gas expensive isn't crude. It's that crack spread, the refinery scarcity. And that's high because the road is still blocked. You can talk crude down to $68. You cannot talk a refinery into finding gasoline that isn't arriving.

So instead the administration yells at the oil companies for "gouging", which polls beautifully and accomplishes nothing, because there is no gouging to find. Only scarcity.

"Contrary to equities, which can be influenced by sentiment over long periods of time, commodity markets are rooted in physical reality. Reality was catching up to the president."

— Ron Bousso, Reuters

That's the trap.

A war he can't cleanly end, an election that punishes the fallout, and no real offswitch. And beneath it all sits the hardest knot of all: Iran's entire prize from this war is control of that strait, the right to charge every passing ship a toll. It's their ultimate insurance against ever being attacked again. The U.S. has flatly called a toll a nonstarter. But as HFI points out, there's no middle ground on a chokepoint. You either control it or you don't. Which is exactly why this conflict is nowhere near as finished as that calm price wants you to believe.

Add it all up, and only one thing is holding the price down: a bluff and a crowded bet.

Line it all up in one place, because once you see it together, it's very hard to shake.

The ships say the road is still closed. The stockpiles are draining at a pace not seen in decades, into the tightest oil-and-gasoline market on record. The refiner's cut is at an all-time high, a flashing scarcity light, whispering that crude "should" be near $100-125, not $68. The crowd has bet against oil about as hard as it ever has, leaving almost no one left to sell, and a coiled spring if it turns. China, the one buyer big enough to keep the world loose, is running low on its own fuel and has quietly begun buying again. And the politics have wound a clock around the whole thing.

Every honest instrument points the same way.

The only thing pointing the other way is the headline price of crude itself, and it's being propped up by the two flimsiest forces in all of markets: a politician's talk, and a one-sided bet.

This isn't a prediction. It's a coiled spring, and a cheap way to bet on it.

Now, I want to be careful and honest with you.

This is not a confident call that oil is about to rocket tomorrow.

It's something more disciplined than that, and frankly more useful. It's a setup where the possible reward badly outweighs the risk.

A trap has been laid for every trader betting on lower prices.

That trap springs the instant the physical market tightens up again.

And the trigger for that is China walking back into the room as a buyer, which its own draining fuel supplies are steadily pushing it to do.

When that happens, a crowd that has bet everything on lower prices will be forced to lunge the other way, all at once.

The downside is small, because the bet against oil is already so crowded it can't fall much further. The upside is the snap-back.

So you don't have to be a hero and catch a falling knife.

The smart version is to buy cheap insurance on the possibility of oil rising, the way you'd buy an umbrella on a sunny day precisely because everyone swears it'll never rain, which is exactly what makes the umbrella cheap. You spend a little to be covered. And if the storm comes, you're the one who stays dry.

The honest answer is that nobody knows the timing.

Only the setup.

The trigger is China, and China is a black box that may deliberately drag its feet, because there's a cold logic to letting the whole world grow desperate before you stroll back in.

A coiled spring can stay coiled far longer than you'd ever guess.

Which is the entire reason you buy the cheap umbrella instead of betting the house.

The road is blocked, but the price is pretending it's open. Everything else, the refiner's cut, the crowded bet, the giant deciding when to walk back into the room, is just the grown-up detail underneath a very simple, very stubborn lie.

Cheers -

PriceTrader